As a successful property investor and as someone who has done their time in the trenches of the market, people expect me to side with the “Harden-up Kids” brigade – with the people who think that the only thing young people need to help them buy a house is a teaspoon of concrete and a lecture.

But I don’t.

In fact, I know first hand that kids these days are facing a very different and very difficult property market. I’m not here to take sides, but I do think someone needs to lay out the cold-hard facts and bust a few of the myths doing the rounds.

As an investor, and economist, I guess that someone is going to be me.

So that’s what this special report is all about. I know we’re all busy, so here’s the Twitter thesis:

There’s so much to get our heads around, I’ve had to break it into three parts:

Part 1 – (Today) Is it harder to buy a house than it used to be?

It’s never been easy, but all the data suggests that it the kids aren’t gutless whingers after all.

Part 2 – (Tomorrow) Why are house prices so expensive?

The Five Disruptions that have taken property prices to their current level (and how to play them to your advantage).

Part 3 – (Thursday) Whaddya going to do about it?

Some big picture thinking and some practical advice to help young people get ahead in a market like this.

This special series is essential reading if you’re a young person looking at buying a house or becoming a property investor. Stay tuned.

Some of this is going to blow your mind. Some of it is going to make you angry. But my real hope is that some of it prepares you for real financial strength, independence and freedom.

Let’s get into it.

Housing affordability is tearing this country apart.

We’re supposed to be one of the wealthiest nations on earth, but hundreds of thousands of people feel like they can’t get a stable roof over their heads. Where did we go wrong?

Affordability affects everybody, but lately this has descended into a slanging match between boomers on one side and millennials on the other. Some young people say baby boomers wrecked the property market. Some boomers say that young people are wasting all their money on iPhones and café breakfasts and need to harden up.

Battle lines are drawn through the Sunday papers.

But don’t buy into it. A lot of boomers made money in property. A lot of them didn’t. If you’re a boomer trying to get into property today, you’re facing the exact same challenges that young people are.

I know it’s fun to throw insults around the Internets, but don’t let them suck you into it. This isn’t mum and dad versus the kids.

This is YOU versus the GAME.

And the game has been stacked against you.

Let me show you how.

This might sound like a stupid place to start, but there are no simple answers in economics. So, at the risk of sounding like a twit,

“Yes, houses are exxy.”

If we take a look at our capital cities, there is a growing concentration of ‘million dollar suburbs’ in our inner-cities. This heat map here shows suburbs with a median house price over $1m, and you can see that within 20km of the Sydney CBD, it is very hard to get a house for less than a million bucks.

But this isn’t just about the top end of town. The number of cheaper homes in the market has been falling too.

This chart shows the proportion of homes for under $400K in our capital cities. It’s now fallen under 20%, and its sinking fast.

In places like Sydney and Melbourne, the picture’s a lot, lot worse.

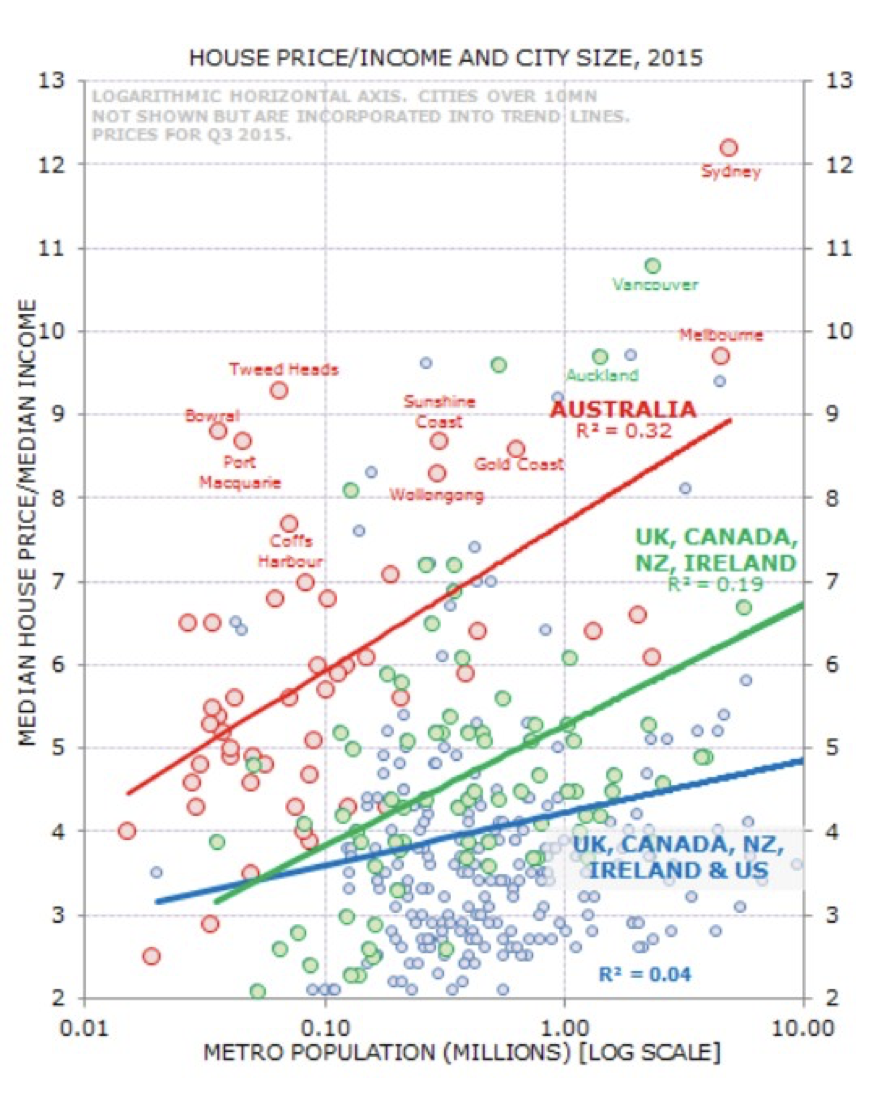

This isn’t just about our capital cities either. On a ratio of prices to incomes, most of our cities are expensive on a global scale. Australian cities are in red here – other western Anglo cities in blue and green.

Australia is expensive on this scale. Sydney and Melbourne are there of course, but so is little ‘ol Tweed Heads, Coffs Harbour and Bowral.

They’re lovely places to live, sure, but you do have to wonder when they’re ranked as some of the most unaffordable cities in the world…

Again, this might sound like a stupid question, but in economics we can’t just talk about expensive. We have to ask our selves, expensive relative to what?

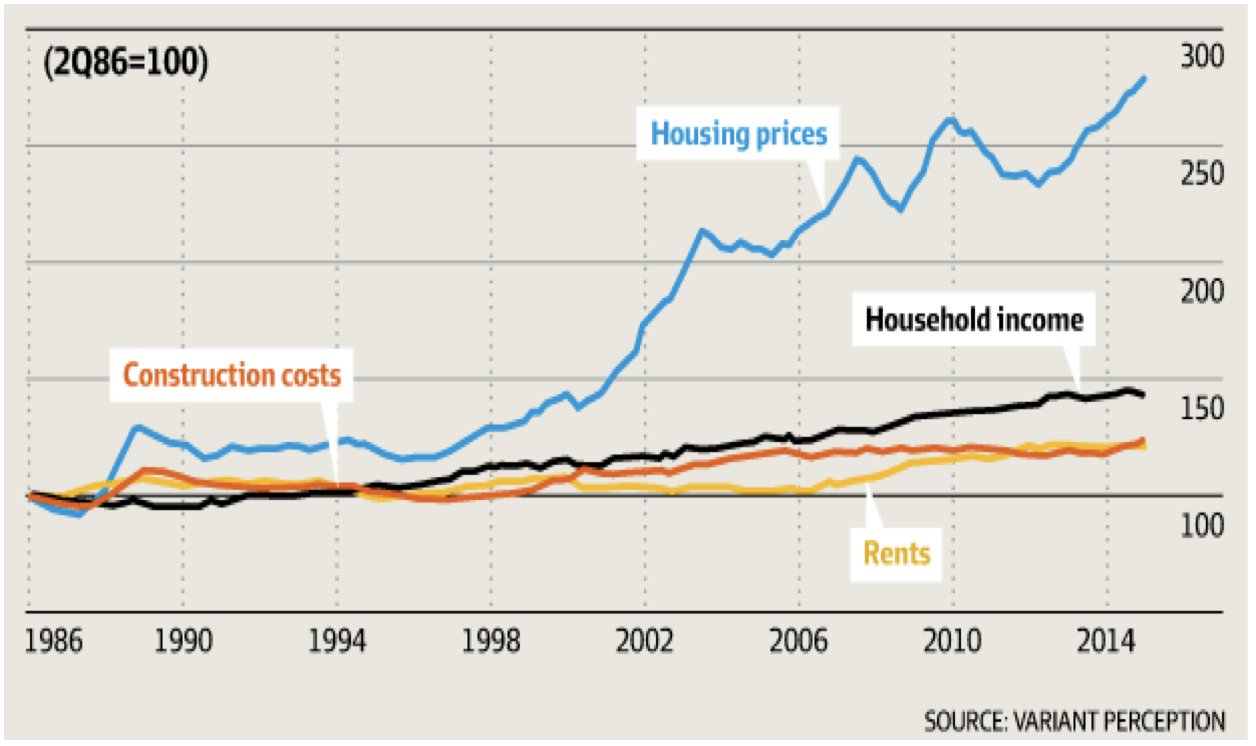

That said, it is kinda true that house prices are expensive relative to everything! That’s what this chart here shows.

This compares house prices (the blue line) with household income (a proxy of purchasing power), rents (the return on the asset) and construction costs.

You can see that relative to these “fundamentals”, house prices have been growing very quickly, with a structural break kicking in around 2000. (Keep that date in mind, we’ll come back to it.)

Long story short, house prices are expensive, no matter which way you cut it.

(Nobel Prize for Economics Committee, I await your call.)

I’ve read a few commentaries recently saying,

“Sure, houses are expensive, but they’ve always been expensive, and they’ve always required sacrifice. That’s the problem with kids these days –they’re just not prepared to do the hard yards. Back in my day, I had to buy five houses before breakfast, crawling on my hands and knees through the trenches of the Boer War…”

So, myth or fact?

This is actually an interesting one. While it is true that house prices have risen, interest rates have been on long downward run, making mortgage repayments easier to handle.

So how do they balance out?

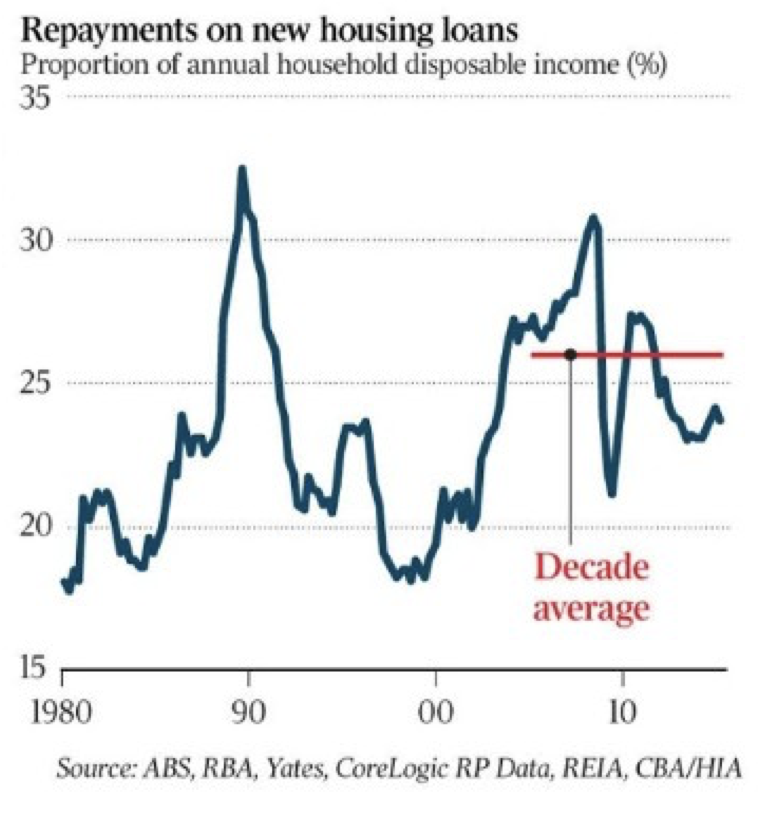

First up, it is true that falling interest rates have made things easier. And if you look at the proportion of the average household budget that’s going towards mortgage repayments, it is currently around the long-run average.

So, purely in terms of mortgage repayments, it is maybe slightly harder to buy a house now but not by a huge amount.

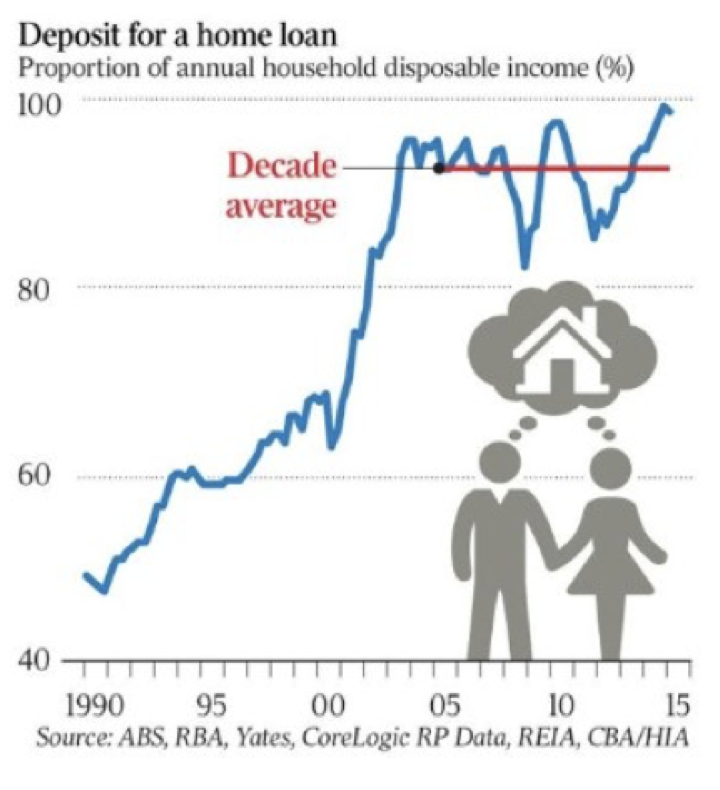

The thing is, though, that interest rates don’t help you with your deposit, and it is the deposit hurdle that’s keeping a lot of people out of the market.

If you look at how much of the household budget is required to stump-up for a deposit, it spiked (again, around 2000), and is currently around twice the levels seen in 1990.

That’s another way of saying that it is twice as hard to put together a deposit as it was twenty-five years ago.

To me, the evidence is pretty clear. It is harder to buy a house now than it used to be.

This stereotype plays well in the tabloids, but I don’t see all that much truth in it (and certainly not in my kids, or the kids I work with!).

But we can test it against the data. We can compare the spending patterns of the 25-34 year-olds of today with the spending patterns of that age cohort back in 1984.

What it shows is that on most measures, young people are actually more frugal than they used to be.

The food spend is down from 14% to 10% of income. Recreation is down a smidge. Even the alcohol spend is down from 2.6% to 1.9%. (See? Soft!)

In fact, the only area eating up more of young people’s budget these days is housing costs!

So, this idea that young people are just too soft to make the sacrifices required to buy a house just doesn’t seem to stack up.

One of the things the above analysis ignores is the way our cities have evolved over the past 30 years.

Back in my day, when our cities didn’t sprawl quite as far and transport infrastructure was fresh, commuting wasn’t such a drag.

However, these days, with some of our capitals the size of small European states, commuting has become a big deal.

This is a hidden cost in buying a house.

Say you find an ‘affordable’ house, right on the city fringes. However, it takes you two hours each way to commute to work.

The cost and impact on your life is a lot bigger than the house’s price tag suggests.

In addition, over the past 30 years, while our cities have sprawled outwards, economic activity and jobs growth has remain centralised. 60% of employment growth in the past five years has been in the inner city, while 60% of population growth has been in the outer suburbs. That’s pretty much the exact opposite of what you’d want.

Put those together and you have growing commute times, and years lost in traffic.

You might get your cheap house, but it will cost you in lost leisure time (and petrol, and on road costs…)

Getting angry yet?

As prices slip out of reach, home-ownership rates are falling, particularly for younger people.

Home ownership rates for people aged 25-34 have fallen from around 40% in 2002 to less than 30% in 2014.

The only cohort that hasn’t seen a decline in ownership rates is the 65+ bracket.

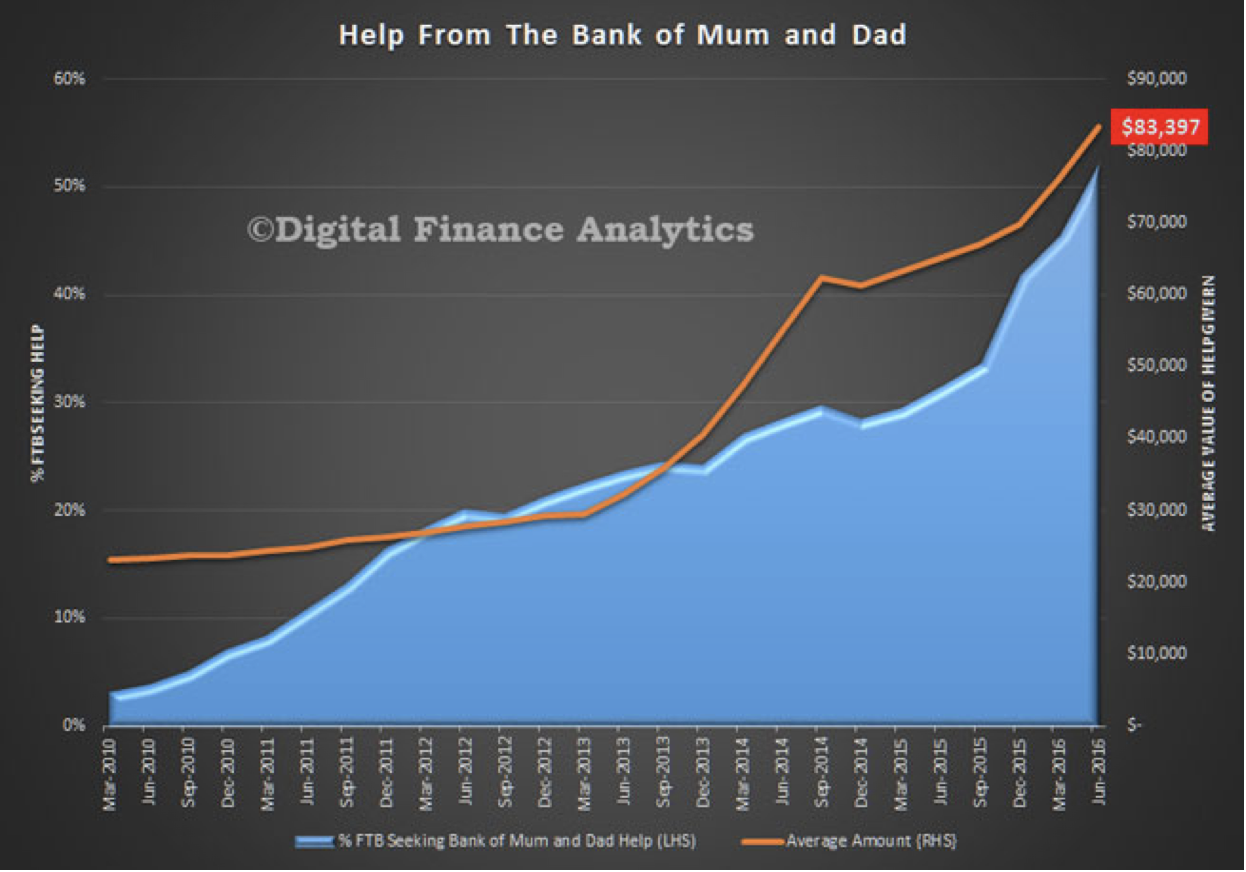

With deposit costs being the major hurdle to home ownership, more and more young people are borrowing from the “Bank of Mum and Dad.”

According to survey work by Digital Finance Analytics, over 50% of first-time buyers borrowed money from their parents.

This phenomenon was practically unheard of only as recently as 2010. Since then, the market has changed in a dramatic way, with more and more people needing family help to get into the market.

Not only are more people borrowing from their folks, they’re borrowing more as well. The average amount has spiked from under $30K five years ago to over $80K now.

This has profound implications for inter-generational equality. I don’t think we want to get to the situation where you have no hope of getting a house unless you parents have wealth they can lend you.

At the same time, older generations are scrabbling to provide for their own retirement. We don’t want to force older people into choosing between the retirement they deserve and the house their kids need.

Nobody is winning in this scenario.

Taking all the data I’ve laid out together, it does seem that, on-balance, it is harder to buy a house now than it used to be, and that is putting pressure on people across the social spectrum.

Now that we have some sense of the shape of the problem, we’re in a position to develop some strategies to solve it – even profit from it.

However, before I can give you some practical, on-the-ground advice (which I’ll do in Part 3), we need to understand why the property market has evolved the way it has.

And so tomorrow, in Part 2, I’ll show you the five big disruptions that have totally transformed the property market in recent years – transformations that have actually made it structurally biased it against young buyers.

It’s essential reading.

Se you tomorrow!

Dymphna.