Here’s some talking points next time someone throws that “highest household debt in the world” line at you…

One of the themes doing the rounds at the moment is that Australian households have too much debt.

This is the Achilles’ heel of Australian property. Aussie households are over-leveraged, and when things sour, they’ll be in real trouble.

The bubble will pop, house prices will crash, and we’ll all have egg on our faces and muck on our shoes.

Obviously, you’ve probably guessed what I think about this.

But first up, yes, Aussie household debt, relative to incomes, is one of the highest in the world. We’ve got a lot of debt.

Is it necessarily a bad thing?

Well, obviously less debt is better than more, but the real question is, is the debt sustainable?

In that way, simple stats about how much don’t really help us. They don’t tell us all that much.

First up, a lot of the arguments about debt are a bit circular. There’s a bubble because we have too much debt. The debt is unsustainable because its been used to buy houses and house prices are unsustainable. Therefore when the bubble bursts the bubble will burst.

It’s not clear to me that house prices are unsustainable. I’ve written a lot about the fundamentals driving the property market right now, and how we’re seeing very different outcomes across the country, but long story short, I just don’t accept the idea that house prices are unsustainable on face value.

So I’m ok with people using debt to buy houses. (I’ve been known to do it myself from time to time.)

So then the question is who is buying the houses?

A lot of people point to the US experience, where people who should never have been getting loans were getting loans. There were the infamous NINJA loans (No income, no job, no assets).

When these NINJA loans went sour, that’s what triggered a collapse in house prices (though I’ll note that house prices have since recovered in the US and are heading north again).

So is there a trigger in Australia like these NINJA loans?

If there is, I don’t know about it. Some people like to point to mortgage-broker originated loans. The idea that mortgage brokers are helping people get loans that they really can’t afford.

There’s no way of knowing how true this is, but I’d have to think it’s pretty marginal. Maybe some mortgage brokers are massaging the numbers and loading people up with another $100,000 or $200,000 over what they can truly afford.

But even if this practice was wide-spread, which I doubt it is, we’re not talking about loading NINJAs up with half a million dollar’s worth of debt, with no foreseeable way of paying it back.

We’re talking totally different scales.

The other point is that America had no-recourse loans. So if you couldn’t pay your mortgage, you just handed in your keys and walked away. The bank couldn’t touch your assets or put any more claims on you.

This created some perverse incentives. What was the harm in loading yourself up to the eyeballs in debt? If it paid off, you pocketed the money. If it went sour, well, you lost your deposit, but beyond that, it was the bank’s problem.

Combine that with the NINJA loan phenomenon, and you have a recipe for an explosion in unsustainable household debt.

In Australia, on the other hand, we have full-recourse loans, so you have to think a lot harder about the debt you’re taking on.

Sure, there are some stupid people out there. But I’ll take a lot of convincing to believe that everyone in the Australian mortgage market is stupid.

So all these parallels to the US market… I’m not really buying it.

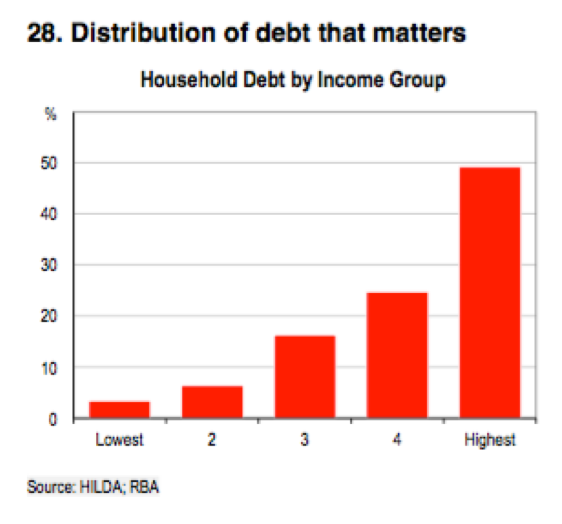

The other point that’s worth making is that most debt in Australia is held by higher income earners.

This chart comes from Paul Bloxham at HSBC. It shows how much of our household debt is held by each income category.

As you can see, almost half of our debt is held by our highest income earners – the top 20%

The bottom 40% – those most vulnerable to unforeseen events and those with the thinnest buffers – they hold less then 10% of our household debt.

Or put it another way, three quarters of our household debt is held by the top 40% of income earners.

Any way you cut it, the point is clear. The people who hold the most debt in Australia are the ones most able to pay.

That should make us relatively relaxed about it (but it doesn’t soothe most people out there it seems.)

The other point, which is an interesting one, is that most rental properties are held privately in Australia. We don’t have a large corporate property sector.

That means that the debt that is held by corporations in other countries, is held by private hands here.

As a result, our household debt figures tend to be over-stated (and corporate debt under-stated).

So to recap, yes, high household debt can be a problem. But when you dig into Australia’s debt, it doesn’t look like we’re a national or irresponsible children throwing caution to the wind.

We have to think hard about the debt we take on, and most debt is held by those most able to pay.

So alert, but not alarmed.

This has been a public service announcement from Dymphna Boholt.

Are you worried about our debt levels?