If history is a guide, then people are panicking about nothing.

A few people in the media are now talking about house prices falling 30%.

Is this unusual?

Well, no. People talk about this all the time. Like every six months or so. People talking about 30% falls is incredibly common.

But what about falls of 30% in the property market. How often does that happen?

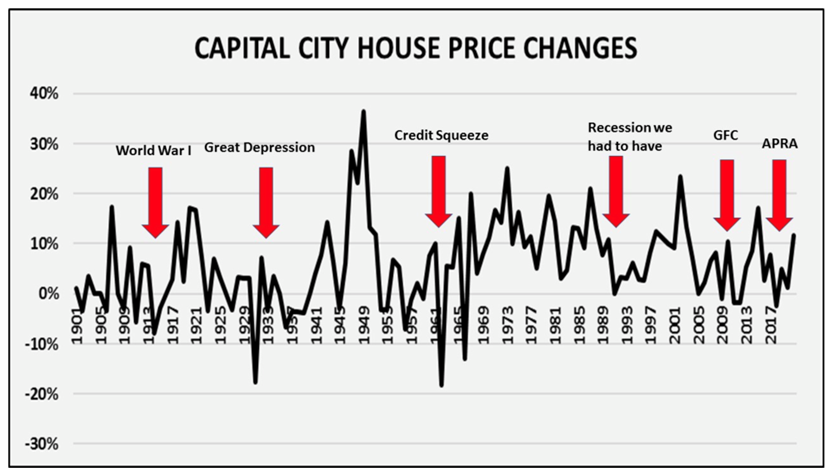

Well, I dug into the history books, and here’s a list of all the times since Federation in 1901 that property prices have fallen by 30% or more:

That’s it. It hasn’t happened. It’s never happened.

Take a look at the chart if you don’t believe me:

The thing to note here is that falls of any magnitude are incredibly rare. Even during the GFC – one of the most calamitous financial events of my lifetime – Aussie property prices fell less than 5% peak-to-trough.

So historically speaking, falls of any magnitude are incredibly rare.

That’s not to say they can’t happen. They just generally don’t.

And while falls of any kind are rare, falls of 30% are just unheard. It just doesn’t happen. Maybe we got close on a peak-to-trough basis during the Great Depression. But that was the single most epic financial meltdown in the history of the world.

So look, that’s the first point. If people are talking about 30% falls, they’re talking about something happened which has almost never happened in the history of Australia.

The second point to note here is that when you look through those rare periods where prices went backwards.

Sometimes they occurred during recessions and negative economic growth, but not always.

They did not occur during periods of high inflation, like the oil shocks of the 1970s.

No, the common factor is a squeeze on credit.

House prices tend to fall when credit becomes in short supply.

And I’m not talking about interest rates here.

You can map house prices against interest rates and there’s no real connection. Interest rates tend to go up with inflation and houses prices tend to go up with inflation too.

Anyway, house prices tend to fall when credit tightens.

That is, when the availability of credit dries up. So the credit squeeze of the 60s, the recession we had to have, the GFC and the APRA squeeze of 2018.

It’s not the price of credit (i.e interest rates) here that matters. It’s the availability of supply.

And the supply of credit tends to dry up either through explicit government policy (e.g APRA squeeze) or when global financial markets are in meltdown (e.g GFC).

If you’re worried about house price falls, this is what you’ve got to watch for.

It’s not interest rates in and of themselves. It’s the availability of credit.

And property price falls of 30%? That’s a different story altogether. It’s theoretically possible.

But if history is any guide, it just doesn’t happen.

DB.